Is Travel Insurance Needed for a Visa What Travelers Should Know

Insurance

|

April 21, 2026

Traveling internationally opens a world of adventure, but if you plan to apply for a visa, you might be questioning whether travel insurance is necessary. The answer often depends on your destination. While some countries explicitly require proof of travel insurance as part of the visa application process, others do not. This requirement usually arises from the need to ensure that visitors have financial coverage against unforeseen medical emergencies or other travel-related incidents. Familiarizing yourself with these requirements is crucial; neglecting this essential step could complicate your visa approval and negatively affect your overall travel experience.

Traveling internationally opens a world of adventure, but if you plan to apply for a visa, you might be questioning whether travel insurance is necessary. The answer often depends on your destination. While some countries explicitly require proof of travel insurance as part of the visa application process, others do not. This requirement usually arises from the need to ensure that visitors have financial coverage against unforeseen medical emergencies or other travel-related incidents. Familiarizing yourself with these requirements is crucial; neglecting this essential step could complicate your visa approval and negatively affect your overall travel experience.

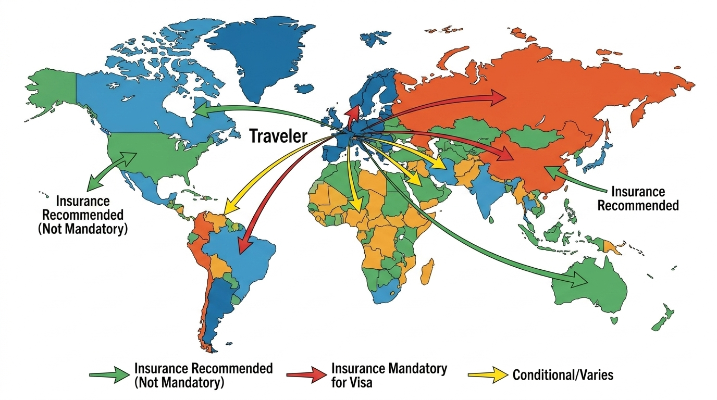

Visa insurance requirements vary significantly from one country to another. For example, European countries in the Schengen Area have strict mandates that travelers must present travel insurance covering a minimum of €30,000 for medical expenses and repatriation. Conversely, other locations might not impose formal insurance requirements but still strongly advise obtaining it. It’s vital to research the particular regulations related to your travel destination to avoid unexpected issues at the time of application.

In this guide, we will delve deeper into the travel insurance landscape associated with visa applications. We will cover the implications of these requirements and how they directly influence your visa approval process. Furthermore, we will highlight common pitfalls that travelers encounter regarding travel insurance. From selecting a suitable policy that meets essential coverage to understanding when and where to submit your insurance documents, we aim to equip you with all the necessary information to make informed decisions. By the end of this article, you will possess a clear understanding of travel insurance's role in your visa application journey, allowing you to travel confidently and with peace of mind.

Is Travel Insurance Needed for a Visa?

Travel insurance is frequently a critical requirement when applying for visas. Numerous countries require that travelers hold valid travel insurance to obtain their visa. For instance, countries such as those in the Schengen Area, Australia, and Canada expect applicants to furnish proof of insurance that covers medical expenses and repatriation as part of their visa application. Not providing this documentation can lead to visa denials.

In contrast, countries such as the United States don't formally require insurance, although possessing it is highly recommended to enhance personal safety and reduce potential risks. Visa approval can greatly depend on complying with these insurance mandates. For example, a traveler aiming to enter Germany needs to present insurance documentation that covers at least €30,000 in medical expenses; failing to do so can result in an outright rejection of the visa application. Similarly, those applying for student visas to Australia without travel insurance might face significant delays or even outright denials, reinforcing the idea that proper coverage is essential for a smooth visa process. Overall, comprehending specific requirements in various countries regarding travel insurance can substantially affect the likelihood of securing your visa.

Why Do Some Countries Require Travel Insurance for Visa Applications?

Governments worldwide have instituted travel insurance requirements for diverse visa applications, emphasizing safety, accountability, and financial security while accommodating international visitors. Below are significant reasons behind these mandates.

Medical Emergency Protection

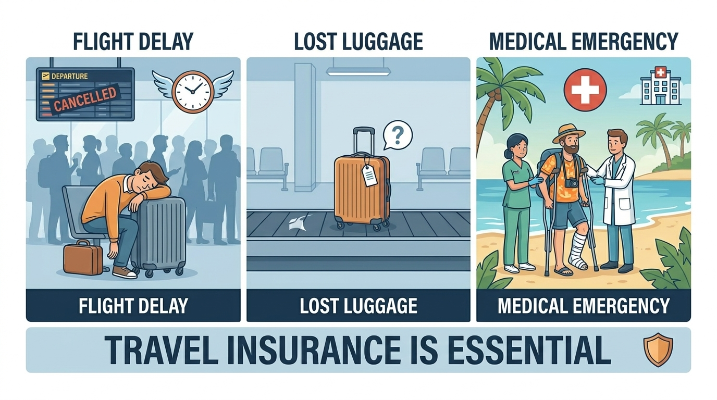

Primarily, many countries require travel insurance to safeguard visitors in case of medical emergencies. An unforeseen situation can arise, such as a traveler becoming ill or having an accident abroad. For instance, consider a tourist experiencing a heart attack while hiking in the mountains of Peru. Without insurance, the steep medical bills and potential hospital costs could quickly escalate, creating a financial burden. Travel insurance offers a critical safety net, ensuring that visitors have access to necessary medical treatments without annihilating their finances or overwhelming local healthcare systems.

Reducing Public Healthcare Costs

Government-imposed insurance requirements also aim to alleviate the financial burden on public healthcare systems resulting from uninsured foreign visitors. When an accident occurs, like a traveler being injured in a traffic incident in Thailand, the local hospitals often absorb the expenses if the injured party cannot pay. By mandating travel insurance, countries can mitigate the strain on taxpayers and encase that visitors are contributing to their healthcare systems in the event of medical emergencies.

Ensuring Financial Responsibility of Visitors

Another vital reason is to ensure that visitors are financially accountable for their actions while abroad. If a traveler inadvertently damages property or injures someone, travel insurance allows the insurer to manage the associated costs, preventing complex legal matters and potential financial liabilities for the host country. For example, if a tourist accidentally damages a rental car, suitable insurance coverage can provide the necessary protections.

Emergency Evacuation and Repatriation Coverage

Finally, many nations require travel insurance to guarantee coverage for emergency evacuations and repatriation. Imagine a scenario in which a natural disaster occurs while travelers are in Japan, like an earthquake. Travel insurance could assist in covering the expenses associated with evacuation, allowing individuals to return home safely without incurring exorbitant costs. This not only protects tourists but also enables countries to manage crises effectively.

In essence, travel insurance is not merely bureaucratic red tape; it serves as a crucial protective measure that fosters safety, accountability, and mutual benefits in international travel.

Notable Requirements

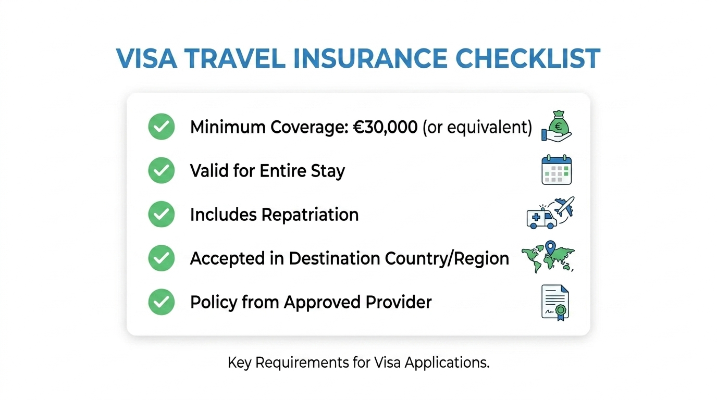

Among the most significant regions is the Schengen Area, which mandates that travelers present insurance documentation providing a minimum of €30,000 coverage for medical emergencies. This measure guarantees that health-related fiscal support is easily accessible. Additionally, Cuba requires travelers to maintain valid international health insurance for the entire duration of their stay, just as does Turkey, which stipulates a minimum of $30,000 in coverage.

Meanwhile, the UAE enforces similar regulations, necessitating that visitors have valid health insurance. However, it is noteworthy that countries like Australia and the USA do not require travel insurance but recommend obtaining it to navigate possible healthcare difficulties.

Travelers ought to be cognizant that visa requirements, including travel insurance mandates, frequently change. Therefore, consulting updated requirements from official consular resources or websites before embarking on international excursions is vital for ensuring a smooth travel experience.

Is Travel Insurance Mandatory for a Schengen Visa?

Acquiring a Schengen visa requires specific travel insurance that adheres to particular standards.

Required Coverage Amount

Travelers must ensure their policy provides a minimum coverage amount of €30,000 to cover medical expenses and emergency hospitalization during their stay in the Schengen Area.

Medical and Emergency Coverage Requirements

The travel insurance policy must encapsulate medical emergencies, encompassing accidents, illnesses, and repatriation for medical reasons. Furthermore, it should extend coverage for emergency dental treatment, ensuring comprehensive care.

Proof of Insurance Needed for Application

When applying for a Schengen visa, applicants must include proof of insurance alongside their application. This proof usually consists of a certificate or policy document outlining the coverage details and confirming they meet the requisite standards.

Consequences if Coverage Does Not Meet Requirements

Failure to provide adequate insurance coverage may lead to visa denial. Inadequate insurance could also result in substantial out-of-pocket expenses during emergencies, underscoring the importance of adhering to these stipulations when planning travels to Schengen countries.

Countries Where Travel Insurance Is Usually Not Required for a Visa

Travel insurance is frequently overlooked by travelers heading to popular destinations like the United States, the United Kingdom, Canada, and Australia, where having travel insurance is typically not a visa requirement. While this lack of obligation may seem reassuring, travelers should approach these situations cautiously.

Going without travel insurance leaves you vulnerable to significant financial implications from unforeseen events—such as medical emergencies or trip cancellations. In countries like the U.S., the costs for medical care can be staggering; even a brief hospital stay can quickly escalate into thousands of dollars.

Although these countries generally do not mandate proof of insurance upon entry, many seasoned travelers still choose to buy travel insurance as a precautionary measure. Traveling without insurance could expose individuals to substantial out-of-pocket costs. Thus, while enjoying the ease that comes with less stringent visa requirements, one must weigh the risks of going uninsured. Making an informed decision is vital; those venturing abroad are encouraged to consider their health needs and the financial implications of unexpected occurrences, despite the lack of formal obligations.

What Type of Travel Insurance Is Accepted for Visa Applications?

When applying for a visa, selecting the right travel insurance policy is essential. Accepted policies typically incorporate key characteristics to ensure sufficient coverage while traveling. Here are the crucial components:

- Emergency Medical Coverage: This should encompass unexpected medical costs accrued while abroad, including doctor visits and medications.

- Hospitalization Expenses: The policy must cover expenses incurred from hospital stays, which can be considerable in specific countries.

- Medical Evacuation: In scenarios where professional treatment is needed but unavailable locally, coverage for medical evacuation will transport you to an appropriate medical facility.

- Repatriation Coverage: This guarantees your remains are returned to your home country in the event of death, a requirement for numerous visa applications.

- Coverage Period Requirements: The policy should encompass the entirety of your stay, and some countries necessitate proof of coverage for the precise duration outlined in your visa application.

Travel Insurance Checklist:

- Confirm Coverage Limits: Ensure they meet or exceed the requirements of the country in question.

- Check Inclusions and Exclusions: Comprehend what is encompassed under the policy.

- Validate Emergency Assistance: Verify if 24/7 support is included.

- Read Reviews: Look for credible insurance providers with favorable feedback from travelers.

- Receive Documentation: Make sure to obtain proper certificates for your visa application.

By meeting these criteria, travelers can feel secure in their arrangements and enhance their chances of a successful visa application.

What Documents Are Needed to Prove Travel Insurance for a Visa?

When applying for a visa, travelers must submit specific documentation to demonstrate their travel insurance coverage. Key documents should include:

- Insurance Certificate: The official document issued by the insurance provider, confirming that you hold a valid policy.

- Policy Schedule: Outlines coverage details, including the terms and conditions of the insurance.

- Coverage Summaries: A brief overview of the insured segments, such as medical emergencies, trip cancellations, and theft or loss of belongings.

- Policy Number: Essential for identification, this number allows visa officers to validate that the insurance is active.

- Traveler Details: The documentation needs to consist of the traveler’s name, age, and travel dates to ensure the policy aligns with the visa application.

- Coverage Dates: It's paramount to provide documentation specifying coverage dates matching the intended travel period.

Visa officers typically scrutinize these documents to ensure that the insurance meets the stipulations established by the destination country, affirming that you possess adequate medical coverage and that your travel plans are protected.

What Happens If You Apply for a Visa Without Travel Insurance?

Submitting a visa application without including travel insurance can lead to various negative consequences that could jeopardize your travel plans. Notably, many countries require proof of travel insurance as a condition for visa approval. Without it, there may be delays in the application process as embassies assess the necessity for additional documents, causing a prolonged waiting period—especially problematic when a travel date is approaching.

For instance, a traveler who applies for a Schengen visa without the required insurance might find their application stalled while authorities seek clarification regarding the absence of this essential coverage, resulting in missed flights and accommodation bookings. In extreme circumstances, the visa can be outright denied due to non-compliance with specific requisites—such instances are not unusual and could incur significant financial strain.

Furthermore, even in cases where travel insurance is not strictly mandated, foregoing it exposes travelers to unforeseen risks. Medical emergencies abroad, unexpected trip cancellations, or lost belongings could impose exorbitant expenses. For instance, a traveler who fell ill while visiting Thailand and lacked insurance confronted over $10,000 in medical bills. Thus, the lack of travel insurance could be detrimental not only to obtaining a visa but also to the overall safety and financial prudence of the trip.

How to Choose Travel Insurance That Meets Visa Requirements

Selecting the appropriate travel insurance for your visa application involves several essential steps. Follow this practical approach to guarantee you fulfill all necessary requirements:

Step 1: Check Embassy Requirements

Before securing travel insurance, review the specific criteria set forth by the embassy or consulate of the country you intend to visit. Some locations require a minimum coverage level or specific types of insurance.

Step 2: Verify Coverage Amounts

Ensure your chosen policy meets or surpasses the minimum coverage required by your destination’s embassy. Common requirements include medical expenses, trip cancellation, and emergency evacuation coverage.

Step 3: Confirm Destination Validity

Not all insurance policies are valid everywhere; ensure your selected policy explicitly encompasses your intended travel locations to prevent surprises.

Step 4: Review Exclusions and Limitations

Thoroughly read the policy details to understand included and excluded items. Pay special attention to limitations concerning pre-existing conditions or particular activities.

Step 5: Obtain Proof of Coverage

Once you select a suitable policy, ensure you receive proof of coverage. This document may be essential during visa applications or upon entry at your destination.

Step 6: Ensure Documentation Accessibility

Keep your travel insurance documentation easily accessible during your trip. Having both digital and printed copies handy is essential for emergencies or visa checks.

By adhering to these steps, travelers can procure travel insurance that not only secures their journey but also effectively fulfills visa requirements.

Final Thoughts on Is Travel Insurance Needed for a Visa

In summary, travel insurance can play a pivotal role in obtaining a visa, as many countries stipulate providing evidence of coverage as part of their application process. This article has outlined specific requirements imposed by various countries, dispelling common misconceptions regarding travel insurance. It underscores the importance of understanding different types of accepted insurance and potential pitfalls travelers might face without adequate preparation. Most importantly, potential applicants should prioritize verifying travel insurance requirements through official government resources before submitting their visa applications. This practice ensures compliance with all necessary criteria, thus minimizing the risk of visa rejection due to insufficient documentation. In today’s increasingly interconnected world, being knowledgeable about travel insurance can secure your journey while enhancing your travel experience.

Was this helpful? Share your thoughts